What’s New in the 2026 Model Risk Management Regulatory Landscape?

For over a decade, Model Risk Management (MRM) operated under a predictable, if increasingly strained, regulatory doctrine. Anchored by the Federal Reserve’s iconic SR 11-7 guidance in the US and mirrored by prescriptive compliance checklists worldwide, the mandate for risk teams was clear: if it uses data to spit out an estimate, it is a model, and it needs to be validated frequently.

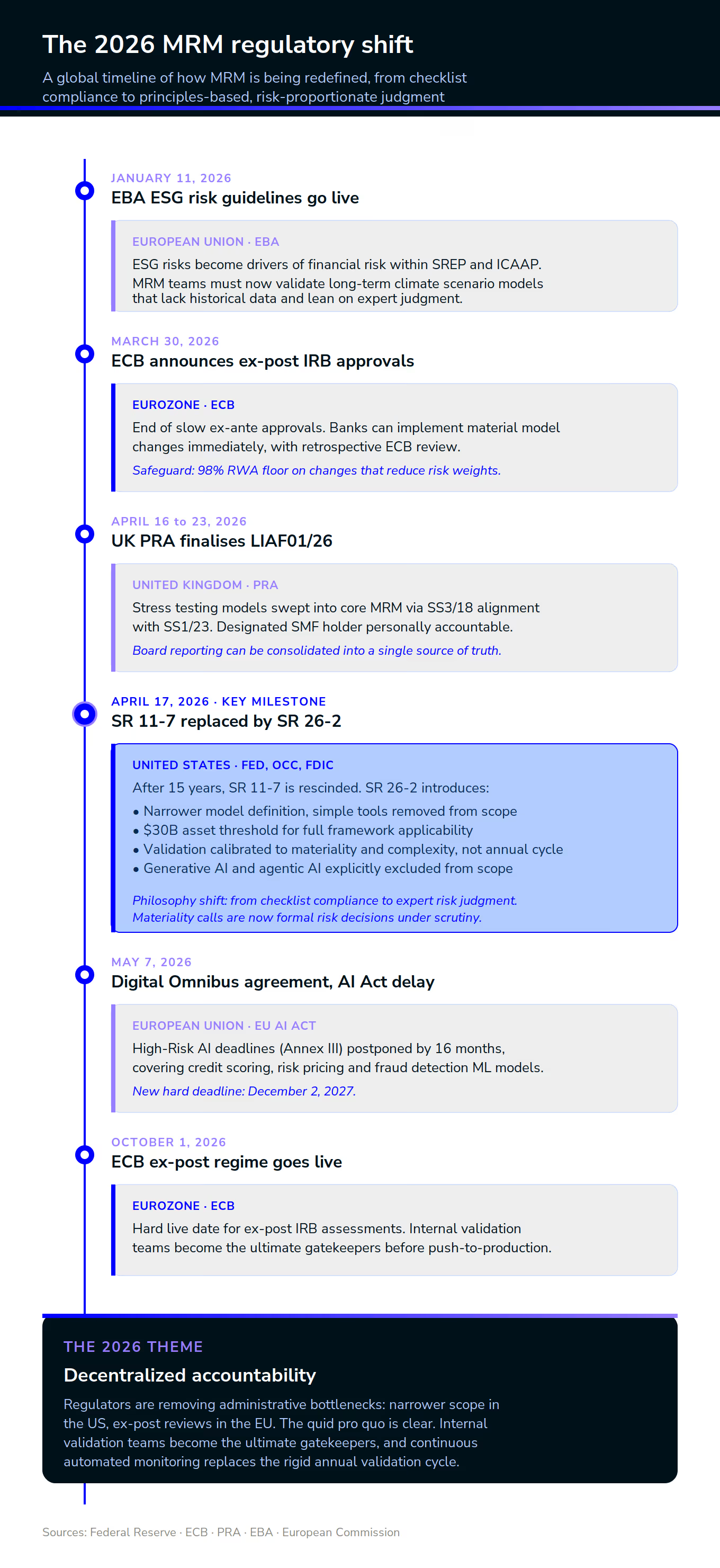

In 2026 a lot is changing

A perfect storm of technological acceleration, regulatory fatigue, and a desire for more agile supervisory frameworks has led to a coordinated global overhaul of MRM. From Washington to Frankfurt and London, regulators have spent the first half of 2026 dismantling rigid checklist compliance in favor of a principles-based, risk-proportionate, and operationally swift approach.

Here is your comprehensive guide to the massive regulatory shifts redefining MRM in 2026.

🇺🇸 The United States: The Fall of SR 11-7 and the Rise of SR 26-2

On April 17, 2026, the US banking agencies (the Federal Reserve, OCC, and FDIC) issued SR 26-2 (Revised Guidance on Model Risk Management), officially rescinding and replacing the fifteen-year-old SR 11-7 framework. The new guidance represents a profound philosophical shift: from a checklist mentality to expert risk judgment.

1. A Narrower, Stricter Definition of "Model"

Under the old regime, bank model inventories ballooned to unmanageable sizes, cluttered with deterministic spreadsheets and simple marketing calculators. SR 26-2 drastically narrows the scope, defining a model strictly as:

"A complex quantitative method, system, or approach that applies statistical, economic, or financial theories to process input into quantitative estimates."

By explicitly removing simple tools from the core MRM scope, regulators are giving financial institutions the license to clean up their inventories. However, SR 26-2 introduces a $30 Billion Asset Threshold. This heavy framework is primarily enforced for Tier 1 and large regional institutions over this limit. Smaller community banks remain under supervisory scrutiny to adopt these sound principles, particularly if they engage in high-risk trading or non-traditional activities.

2. High Stakes for Materiality Assessments

Under SR 26-2, validation frequency and intensity are entirely calibrated to a model’s materiality (exposure and purpose) combined with its inherent complexity. The rigid annual validation cycle is gone. However, labeling a model as "immaterial" to bypass a heavy validation cycle is now a formal risk decision. If that model later contributes to a loss, the initial materiality judgment will face intense regulatory scrutiny.

3. The Generative AI Excluded Gap

Crucially, SR 26-2 explicitly excludes Generative AI and agentic AI from its scope. US regulators have signaled that traditional MRM frameworks are structurally ill-equipped to handle the non-deterministic nature of GenAI, leaving AI governance to separate, specialized risk frameworks and oversight bodies.

Deep Dive: Want to know how to effectively structure your model inventory under these new rules? Read our detailed SR26-2 breakdown in our Yields Insights Article or download our ebook where we navigate SR26-2. Or even better, register for our webinar on the 4th of June 2026.

🇪🇺 The Eurozone: ECB’s Faster IRB Approvals via Ex-Post Assessments

For years, European banks have voiced frustration over the European Central Bank's (ECB) sluggish approval process for Internal Ratings-Based (IRB) credit risk models. Parallel running of old and new models for months waiting for an ex-ante (prior) sign-off stifled innovation.

Announced on March 30, 2026, with a hard live-transmission deadline of October 1, 2026, the ECB has fundamentally transformed this approval mechanism.

1. Moving from Ex-Ante to Ex-Post

Relying on the matured quality of banks' internal control and independent validation functions, the ECB will allow banks to implement material changes to their internal models almost immediately after submission. The ECB will shift its supervisory resources to ex-post (retrospective) targeted reviews and horizontal data analysis.

2. The Safeguard: A Capital Floor

To prevent banks from using unapproved model adjustments to immediately drop their Risk-Weighted Assets (RWAs), the ECB has introduced a prudential floor.

Any material model change that results in reduced risk weights will be subject to a temporary floor of 98% of the old weights (and 100% for model extensions). This floor will only be lifted after the ECB conducts its retrospective review, forcing internal validation teams to be 100% certain of their work before push-to-production.

Read all about it in our latest blogpost on the expected changes in IRB Models by the ECB.

🇬🇧 The United Kingdom: PRA Integrates Stress Testing and Solidifies SS1/23

While the US and EU are looking for ways to streamline or narrow the scope of MRM, the UK’s Prudential Regulation Authority (PRA) is doubling down on its stringent SS1/23 standard (Model Risk Management principles for banks).

Through its LIAF01/26 (Low Impact Amendments Finalisation) policy, published on April 16, 2026, and entering into effect on April 23, 2026, the PRA made small but highly consequential adjustments to further solidify its framework.

1. Stress-Testing Models Swept into Core MRM

The PRA formally updated SS3/18 (MRM principles for stress testing), aligning it directly with SS1/23. This effectively forces UK firms to govern, validate, and document their stress-testing and ICAAP models with the same rigorous independent challenge as core capital models.

2. Streamlining Board Reporting & Accountability

While this looks like an extra burden, the April update actually aims to reduce reporting duplication. By embedding stress testing directly under the overarching SS1/23 framework, the PRA allows firms to combine their board-level reporting into a single source of truth. However, the PRA still firmly enforces that model risk must be treated as a distinct risk discipline in its own right, requiring a designated Senior Management Function (SMF) holder to be personally accountable to the board.

Expert Opinion: Navigating the cross-border complexities between PRA's updated SS1/23 and the new US SR 26-2 requires a unified platform approach. Discover more on the latest update by the PRA of SS1/23.

Beyond the Core Updates: EBA’s Hard ESG Mandate & The EU AI Act

Two massive external overlays are forcing bank MRM teams to run on a multi-track system in 2026:

1. The EBA ESG Risk Mandate (Effective January 11, 2026)

The European Banking Authority's (EBA) final Guidelines on the management of ESG risks have been fully operational for Significant Institutions since January 11, 2026. ESG risks are no longer qualitative disclosures; they are treated as major drivers of traditional financial risk within the SREP and ICAAP processes. MRM teams are now forced to validate highly unpredictable, long-term climate scenario models that lack historical data and lean heavily on expert judgment.

2. The EU AI Act: High-Risk Deferral to December 2, 2027

Following a major political agreement on the Digital Omnibus on AI on May 7, 2026, EU lawmakers officially postponed the deadlines for "High-Risk AI" systems (Annex III). Financial models that use machine learning for credit scoring, risk pricing, or fraud detection have received a 16-month extension, shifting their hard compliance deadline from August 2026 to December 2, 2027. While this gives validation teams temporary breathing room, institutions are expected to use this period to thoroughly embed algorithmic bias controls, data lineage, and human-in-the-loop oversight into their systems.

Summary for Risk Leaders: The Shift to Continuous Monitoring

The overarching theme of 2026 is decentralized accountability. Regulators are handing the keys back to financial institutions. By narrowing model definitions (US) and moving to ex-post reviews (EU), they are removing administrative bottlenecking.

However, the quid pro quo is harsh: Internal validation teams must now act as the ultimate gatekeepers. Because rigid annual validation checklists are a thing of the past, forward-thinking institutions are shifting to continuous automated monitoring. By setting real-time thresholds for data drift and model performance deterioration, MRM teams can catch issues early, aligning perfectly with the ECB’s new ex-post assessment approach and the PRA's unified accountability rules.

In 2026, Model Risk management (MRM) is no longer about compliance; it is about pure, defensible risk judgment.

Automate Your Transition: Transitioning from annual validation checklists to continuous risk-based monitoring requires the right tooling. See how the Yields Model Risk management software automates ongoing performance tracking and data lineage.

About the

Author(s)

Sébastien Viguié is the co-founder of Yields, the first FinTech platform leveraging AI for enterprise-scale model testing and validation. A strong advocate of model risk governance and strategy, he focuses on helping financial institutions embed trust, transparency, and compliance into their AI and model lifecycle. Previously CISO at Yields, Sébastien gained hands-on experience reconciling cybersecurity principles with model risk management and AI governance, a perspective he now extends to emerging regulatory frameworks such as ISO, NIST, and the EU AI Act. Before founding Yields, he worked as a front-office quantitative analyst at BNP Paribas, where he developed a deep understanding of model development and validation in fast-paced trading environments, expertise that continues to inform his pragmatic approach to responsible AI and risk management today.