Blog

News & Insights

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

OSFI E-23 vs SR 26-2: How Canada and the US Are Diverging on Model Risk Management

OSFI E-23 vs SR 26-2: How Canada and the US Are Diverging on Model Risk Management

June 18, 2026

OSFI Guideline E-23: What Canada's New Model Risk Management Rules Mean for Financial Institutions

OSFI Guideline E-23: What Canada's New Model Risk Management Rules Mean for Financial Institutions

.png)

June 18, 2026

Scaling Model and AI Risk Management in Complex Financial Organisations

Scaling Model and AI Risk Management in Complex Financial Organisations

June 15, 2026

What is Model Risk Management? Back to Basics

What is Model Risk Management? Back to Basics

June 15, 2026

hireEZ and Yields: Building Audit-Ready AI Governance for the EU AI Act

hireEZ and Yields: Building Audit-Ready AI Governance for the EU AI Act

June 3, 2026

Ebook: Build vs. buy in Model Risk Management

Ebook: Build vs. buy in Model Risk Management

May 20, 2026

The New IRB Playbook: Preparing for October 1, 2026

The New IRB Playbook: Preparing for October 1, 2026

May 20, 2026

What’s New in the 2026 Model Risk Management Regulatory Landscape?

What’s New in the 2026 Model Risk Management Regulatory Landscape?

May 19, 2026

Mastering SS1/23 in the New Era of UK Model Risk

Mastering SS1/23 in the New Era of UK Model Risk

May 19, 2026

The AI Act Delay Delusion: Why AI Governance is Still a 2026 Priority

The AI Act Delay Delusion: Why AI Governance is Still a 2026 Priority

May 18, 2026

Speeding up IRB models: The Shift to Ex-Post Model Supervision on October 1, 2026

Speeding up IRB models: The Shift to Ex-Post Model Supervision on October 1, 2026

May 18, 2026

Comprehensive Overview of US Banking Laws and Regulations

Comprehensive Overview of US Banking Laws and Regulations

April 24, 2026

Yields Expands into APAC with Atif Khan as Regional Lead

Yields Expands into APAC with Atif Khan as Regional Lead

April 23, 2026

.avif)

Navigating SR 26-2: New technological requirements for model risk management

Navigating SR 26-2: New technological requirements for model risk management

April 22, 2026

Elevating Risk Management to AI Governance at Enterprise Scale

Elevating Risk Management to AI Governance at Enterprise Scale

April 15, 2026

Learnings from MRM implementation at a major Australian bank

Learnings from MRM implementation at a major Australian bank

March 31, 2026

Unlocking the Future of AI Governance and Model Risk: Why We’re Building an MCP Server

Unlocking the Future of AI Governance and Model Risk: Why We’re Building an MCP Server

March 26, 2026

Yields is Now Available on Google Cloud Marketplace

Yields is Now Available on Google Cloud Marketplace

March 26, 2026

Navigating Model Risk in the Age of Agentic AI

Navigating Model Risk in the Age of Agentic AI

March 26, 2026

AI Governance at Scale: Navigating Risk, Regulation, and Geopolitics

AI Governance at Scale: Navigating Risk, Regulation, and Geopolitics

March 26, 2026

From Principles to Practice: Building Strong AI Governance

From Principles to Practice: Building Strong AI Governance

March 26, 2026

Novobanco and Yields: Transforming Model Risk Management for the AI Era

Novobanco and Yields: Transforming Model Risk Management for the AI Era

February 28, 2026

.avif)

.avif)

Five Model Risk Management Trends Defining 2026

Five Model Risk Management Trends Defining 2026

February 10, 2026

Model Risk Management Tooling at Scale: Excel, in-house or Third-party?

Model Risk Management Tooling at Scale: Excel, in-house or Third-party?

February 6, 2026

The Three Lines Of Defence In Model Risk Management

The Three Lines Of Defence In Model Risk Management

February 5, 2026

Yields Named Category Leader in Chartis AI Governance Report 2025

Yields Named Category Leader in Chartis AI Governance Report 2025

January 22, 2026

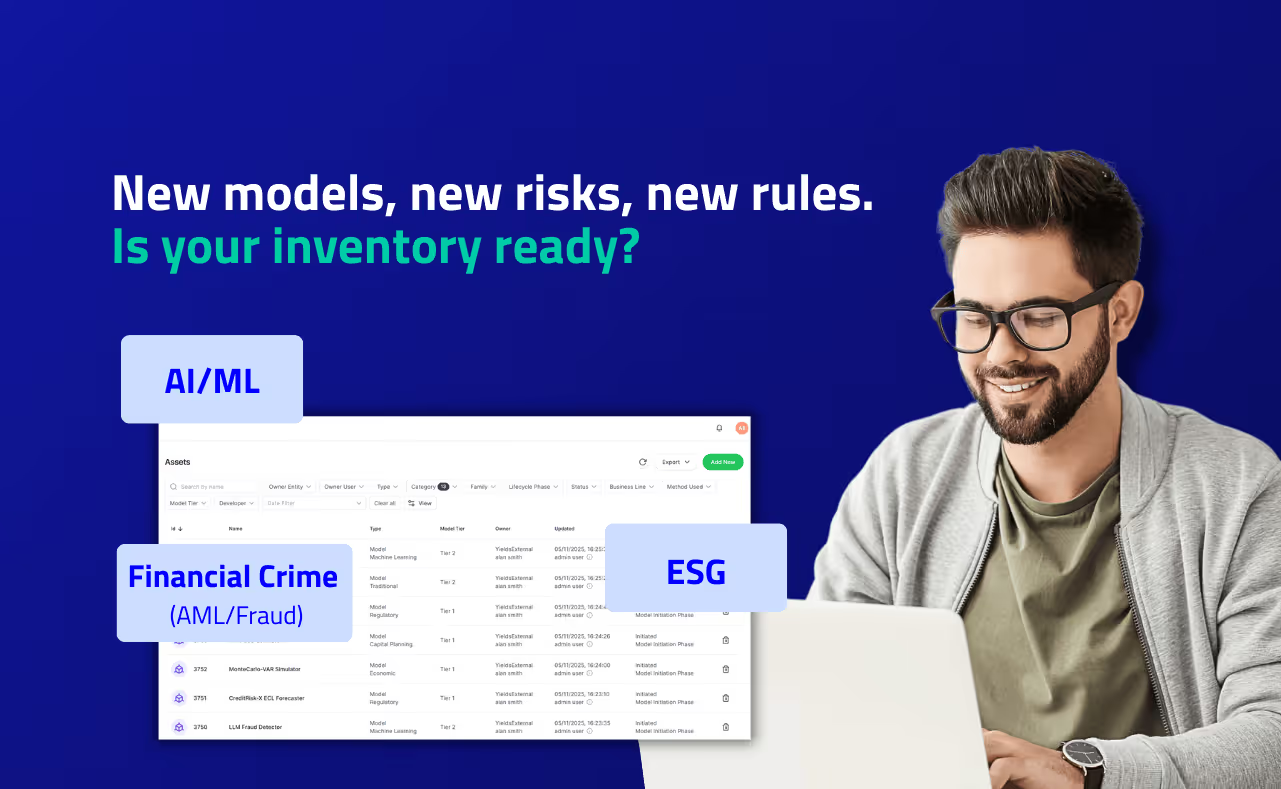

Re-thinking Model Inventories for ESG, AI and Financial Crime

Re-thinking Model Inventories for ESG, AI and Financial Crime

January 14, 2026

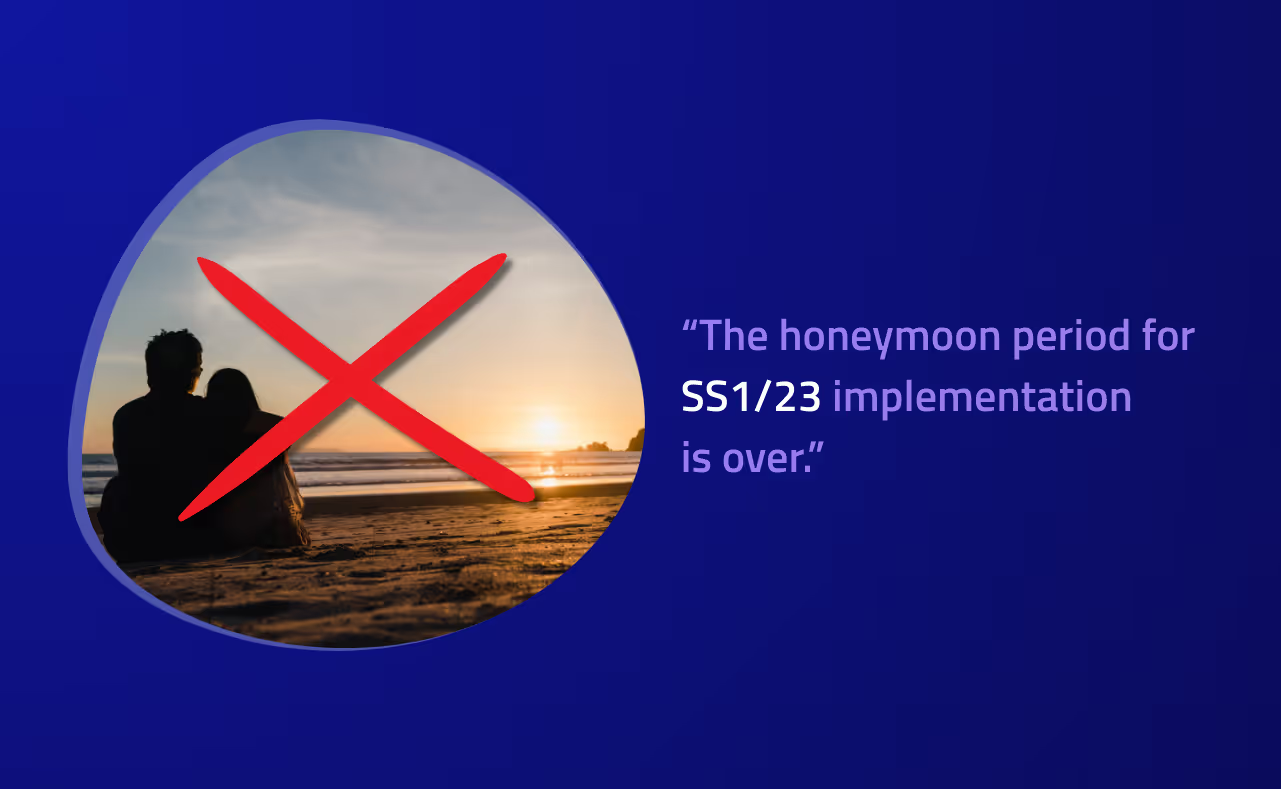

The end of the honeymoon: it´s time to turn PRA feedback on SS1/23 into a scalable model risk strategy

The end of the honeymoon: it´s time to turn PRA feedback on SS1/23 into a scalable model risk strategy

January 7, 2026

Managing AI Risk: Turning principles into practice

Managing AI Risk: Turning principles into practice

December 10, 2025

Key Insights on AI in HR: 20 Essential FAQs

Key Insights on AI in HR: 20 Essential FAQs

November 24, 2025

How HR Teams Can Use AI Safely and Responsibly

How HR Teams Can Use AI Safely and Responsibly

November 24, 2025

Partners Yields and Approach Cyber deliver first successful AI governance fast-track assessment with itsme®

Partners Yields and Approach Cyber deliver first successful AI governance fast-track assessment with itsme®

November 19, 2025

The three levels of AI risk you need to know

The three levels of AI risk you need to know

November 17, 2025

From principles to practice: bringing AI governance to life in finance

From principles to practice: bringing AI governance to life in finance

November 5, 2025

How can you apply AI in HR in a safe and compliant way?

How can you apply AI in HR in a safe and compliant way?

October 23, 2025

Mastering Model Risk Management: Three Success Stories

Mastering Model Risk Management: Three Success Stories

October 22, 2025

Making your Model Inventory work for your organization: An Overview

Making your Model Inventory work for your organization: An Overview

October 11, 2025

Effective AI model risk management: from theory to practice

Effective AI model risk management: from theory to practice

September 8, 2025

Scaling AI Governance: 7 Steps to Get There

Scaling AI Governance: 7 Steps to Get There

September 2, 2025

How Risk Tiering helps you focus AI Governance where it matters most

How Risk Tiering helps you focus AI Governance where it matters most

August 25, 2025

AI Use Case Identification: The first step to effective AI governance

AI Use Case Identification: The first step to effective AI governance

August 11, 2025

Unlock the value of generative AI in financial services

Unlock the value of generative AI in financial services

August 11, 2025

RACI Matrix: Defining Accountability in AI Governance

RACI Matrix: Defining Accountability in AI Governance

August 4, 2025

How to launch a successful AI Use Case discovery campaign

How to launch a successful AI Use Case discovery campaign

August 1, 2025

Monocle Solutions and Yields announce partnership

Monocle Solutions and Yields announce partnership

July 16, 2025

Chartis RiskTech AI 50 Honors Yields for Leadership in AI Governance and Model Risk Innovation

Chartis RiskTech AI 50 Honors Yields for Leadership in AI Governance and Model Risk Innovation

June 24, 2025

AI risk management for data scientists: lessons from finance

AI risk management for data scientists: lessons from finance

June 11, 2025

Navigating regulatory landscapes and enhancing AI reliability across sectors

Navigating regulatory landscapes and enhancing AI reliability across sectors

May 27, 2025

BNP Paribas Personal Finance case study with Yields

BNP Paribas Personal Finance case study with Yields

January 2, 2025

Yields recognized twice as category leader in Chartis Research Model Risk & Validation 2024 Report

Yields recognized twice as category leader in Chartis Research Model Risk & Validation 2024 Report

December 16, 2024

The AI Tightrope: Navigating Risks in the Age of Generative Intelligence

The AI Tightrope: Navigating Risks in the Age of Generative Intelligence

November 11, 2024

Yields named to the 'Ones to Watch' list by Chartis RiskTech100 2025

Yields named to the 'Ones to Watch' list by Chartis RiskTech100 2025

October 22, 2024

The AI Alchemists: How Generative AI is Reshaping Global Finance

The AI Alchemists: How Generative AI is Reshaping Global Finance

October 4, 2024

Why Excel Falls Short for Effective Model Risk Management

Why Excel Falls Short for Effective Model Risk Management

August 26, 2024

Complying with the UK’s New Model Risk Regulation

Complying with the UK’s New Model Risk Regulation

August 22, 2024

Governance, Risk Management, and Compliance for Banking Institutions

Governance, Risk Management, and Compliance for Banking Institutions

November 1, 2023

America First Credit Union: Scaling model risk management

America First Credit Union: Scaling model risk management

September 20, 2023

Automating Model Validation at a Tier 1 Bank

Automating Model Validation at a Tier 1 Bank

September 3, 2023

Automated Testing and Documentation at G-SIB

Automated Testing and Documentation at G-SIB

September 1, 2023

Yields raises €4.8M to accelerate the adoption of its model risk management platform

Yields raises €4.8M to accelerate the adoption of its model risk management platform

June 20, 2023

Model Risk Classification in the Yields MRM Suite

Model Risk Classification in the Yields MRM Suite

June 19, 2023

SS1/23: Model Risk Management Principles for UK Banks

SS1/23: Model Risk Management Principles for UK Banks

June 5, 2023

An Interview with Jos Gheerardyn: Best Practices for Model Governance & Documentation

An Interview with Jos Gheerardyn: Best Practices for Model Governance & Documentation

May 9, 2023

Automated Model Documentation with the Yields MRM Suite

Automated Model Documentation with the Yields MRM Suite

April 13, 2022

Automated model validation: Challenges & Considerations

Automated model validation: Challenges & Considerations

January 13, 2022

Yields, Model Validation Service of the Year 2021

Yields, Model Validation Service of the Year 2021

August 2, 2021

There are no results with this criteria. Try changing your search.